When you set out to get on top of your money and organize your financial life, there is no shortage of methods and solutions that promise big results. It can seem like everywhere you turn – everyone has an opinion about how you should manage your money. Whether the program outlines steps you need to follow or prescribes certain dollar amounts or percentages that you should spend in different categories, it surely promises to fix up your money and get you on the right track. And these systems and solutions on the surface aren’t bad. They give you a place to start, some guidelines, and a base knowledge about personal finances. You may even try one or two of them out, and for a while it seems to be working. But ultimately you find yourself slipping back into old patterns and feeling lost. This doesn’t mean that you’ve failed. The system failed! You just need a system for managing your money that is uniquely you. This is where the 5 key components of successful budgeting come in. If you can build a budget that includes these 5 things, you’re more likely to stick to it and have success in the long run! Let’s look at the 5 key components of successful budgeting you can start to implement today.

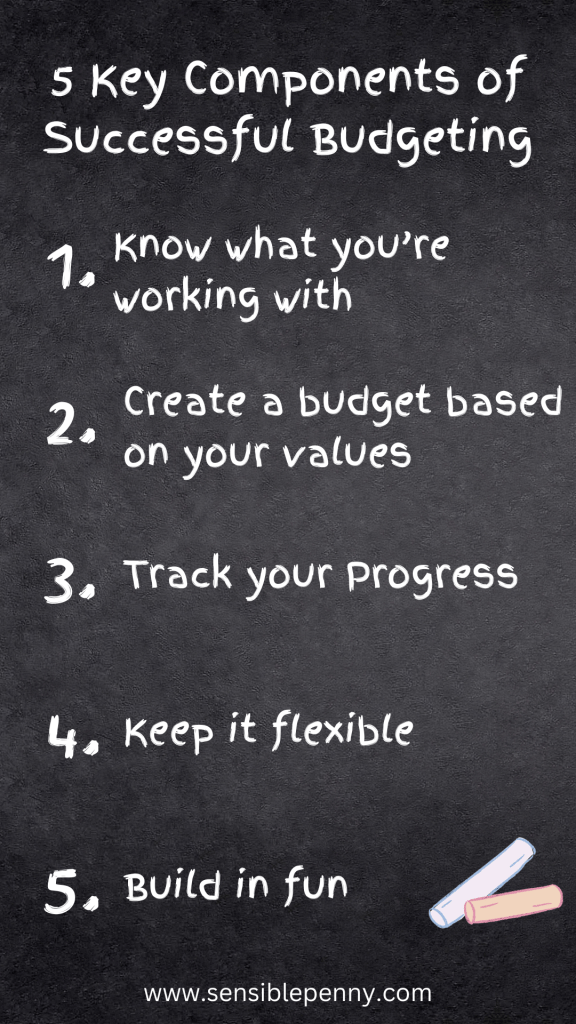

Key Component # 1: Know What You’re Working With

A budget is a great roadmap to building the financial future you envision for yourself. But without knowing exactly what resources you have for the trip; it will be hard to make progress. That’s why one of the 5 key components of successful budgeting is to figure out exactly what you’re working with. To do this, you’ll need to consider what money flows in and out of your account.

First, you’ll want to write down all your income sources. Be sure to include how much you get paid and when. If you’re budgeting with a partner, include their income too. If you are living on variable income, this component can feel difficult. The best thing to do is to look over the last six months’ worth of pay stubs and take an average. Looking at 6 months’ worth of income might feel like overkill, but it gives you more pay periods and can help you even out any seasonal highs or lows you might experience at your job.

Now it’s time to see how money flows out of your account. Start by looking at your fixed expenses. These are the expenses that you must cover every month to keep your life moving forward. Usually, they come on the same day and are for roughly the same amount each month. Include things like rent/mortgage payments, gas/transportation, childcare, your phone and internet bills, utilities, medicine, insurance premiums, and debt payments. It’s helpful to also include an average for spending on food. Look over the last 3-6 months of your spending and make a note of all your fixed expenses.

Finally, you’ll want to identify your flexible and non-monthly spending. Look over your spending for the last 3-6 months again. This time make note of all the expenses you typically face that are not fixed. These expenses include things like eating out, drinks with friends, coffee, shopping, gifts, and entertainment. Any spending that isn’t considered an essential expense will go on this list. Also pull out any bigger bills that you face throughout the year.

Now, compare your income to your spending. This will help you determine how much money you have left to spend, save, and invest according to your values.

Key Component # 2: Create a Budget Based on Your Values

One of the most important components of successful budgeting is to create a budget based on your values. Budgets built of strict rules about how much you can spend in each category don’t take your situation into account. To do this, it’s important to define what’s important to you and be clear about how your spending reflects what you value.

If you’ve worked on Key Component # 1, you’ll have a good idea of what’s coming in and what’s going out each month. Now it’s time to build your values into your budget.

First, you need to identify three to five core values that drive you. To identify them you can use a values list, like Brené Brown’s Dare to Lead List of Values. Read the list and circle words that embody you and that you see as guideposts for your life. Keep reviewing the list until you can narrow it down to three to five core values. If the list method doesn’t resonate with you, it can be helpful to take a critical look at your life and how you spend your time. Often where you choose to spend your time can highlight things that are important to you. Once you’ve identified your values, use these values to help you make money decisions. You’ll be amazed at how doing this keeps things in focus. It can help you decide between two courses of action. It can also help you keep on track.

Key Component # 3: Track Your Progress

Another of the 5 key components of successful budgeting is to track your progress. The next thing you need to do when you ditch the one-size fits all money management systems and build your own is make sure you have a way to track your progress. It’s hard to know where you are and if you’re on track to get where you want to be if you’re not tracking. Creating a reliable system of tracking your money will help. Remember, you want to play to your strengths and keep it simple. Some people LOVE Excel and spreadsheets…others hate them. If you hate them, don’t make it a key piece or your plan. You can track with a pen and paper, with Excel, using your bank app, or using other software or apps. Just be sure to find something you can stick with.

Once you find a way to track, you’ll want to make it a regular process. The best way to do this is to make it a regular appointment on your calendar. Find a time each week where you can spend fifteen to thirty minutes looking at your money. And schedule a money check in appointment with yourself. Be sure to put it at a time where you know you can focus on your money and won’t be distracted. When you sit down during your money check, start by reviewing and tracking your previous week’s spending. Then look to the week ahead. See if there are any bills coming up that you need to pay or if you have any other expenses on the horizon. Doing this can move you from being reactive with your money to be proactive.

Key Component # 4: Keep it Flexible

One of the big issues I have with the one-size-fits-all approaches to budgeting is that often they are rigid. You have to follow a set structure and do things a certain way. But as we all know, that’s not how life works. Things change fast. Emergencies happen. Things beyond our control call for our time, attention, and money. And sometimes, we just forget a bill or expense. This is where flexibility comes in and why it’s one of the five key components of successful budgeting.

One way to maintain flexibility is to budget to a cushion. What this means is instead of budgeting every dollar you earn for a specific purpose; you leave a cushion to give your budget flexibility. This allows you to take on life expenses as they come up and keeps you from feeling like you are constantly going over budget. Having a cushion built in or simply knowing how you will pivot when you have to can be a game changer.

Key Component # 5: Build in Fun

Often when someone starts budgeting, they get so excited and want to see progress immediately. This causes them to over correct and cut out all fun and non-essential spending from their budget. This is a recipe for disaster. A key component of successful budgeting is to build in fun. I know it can seem counterintuitive to keep money in the budget going towards something you enjoy. But it will keep you motivated and on track. Most of the work with budgeting is done for long-run results. While this is good, it can also sometimes be hard to stick to. Building fun into your budget is a helpful way to get some instant gratification while staying involved in the process.

When you build fun into your budget, don’t go crazy. It’s not a license to get reckless with your spending and go off the rails. Instead, look at the resources you are working with and the things you enjoy doing and leave room for those things. If your budget is tight, you may only give yourself $10-$20 a month for fun. And that’s ok. What is important and will help you be successful in your budgeting efforts is that you have some money build in for fun.

Final Thoughts

When you start budgeting, you want to do your best to set yourself up for success. This doesn’t mean it will always be perfect. But it means you’ll have a better chance of sticking with it over time. It’s important to have the right foundation to make this your reality. Start by getting understanding your personal cash flow and getting crystal clear on what you value and why you are setting up a budget in the first place. This helps you make money decisions more easily. It will also be something you come back to when things go wrong. Once you know what you value and why you’re budgeting, it’s important to find a system to track your progress that works for you! Remember to schedule it on your calendar at the same time each week and treat it like an appointment you can’t miss. When you build your budget, don’t forget to build in flexibility and fun. Both will make your budget easier to stick to and will help ensure it is successful. While your budget will be as unique as you are, if you include these 5 components of successful budgeting, and you stick with it, over time you’ll see results.